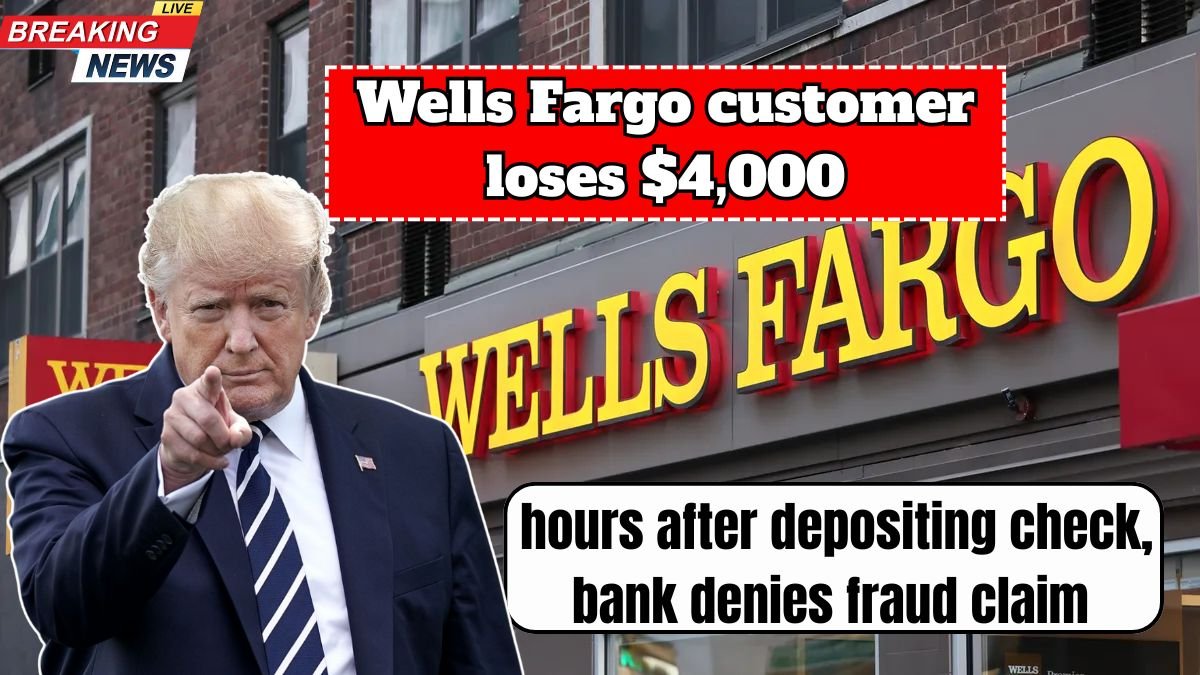

Introduction: It began like any other banking transaction—a normal deposit, a few phone clicks, and what should have been peace of mind. But for Willie Delane, a long-time client in Houston, that typical day turned into a financial nightmare, raising new concerns about bank fraud, customer protection, and accountability.

The Beginning error but A Routine Check Deposit

While Delane, a resident of Houston, Texas, deposited a life insurance check for approximately $10,000 at a bank branch around 1:30 PM on September 15th. She was thinking it seems everything is normal up to this point, the check has been processed, funds will be available in the account, and it and everything should be fine.

But then that night, her peace of mind was shattered. Approximately nine hours later, she received a text message from a number that looked like it was associated with the bank bank,indicating there were suspicious charges on her account.

The Deceptive Message and Call

Following that message, she immediately called bank customer service bank, then number provided in the text. There, a “representative” said that her account had been frozen and a new debit card would be issued. At that moment, she felt relieved; she thought the bank was handling the situation.

But as the night progressed, she discovered: thediscovered thee next day, mordiscovered theday thate than $4,000 was missing from her account. She was shocked she day that she had never authorized such a transaction.

The Bank’s Response Handsashed

When she contacted the bank, they stated that these transactions were “authorized by you,” therefore they could not take responsibility. In other words, the bank denied the fraud claim The issue here is not just the loss of money but the erosion of the trust the customer placed in the bank, abank andd the lack of security that consumers expect.

Legal Complexities and Consumer Rights

This case is significant because it raises the question: when bank-customer interactions occur through mobile or digital means, does that constitute “authorization” bank and”authorization,”or is the customer being deceived?

U.S. There is a regulation called Regulation E, which holds banks liable for electronic fund transfers that were not authorized by the customer. However, in this case, the bank argued that the customer had given consent during the call ev”authorization,”even if unintentionally. In such cases, banks often claim, “You yourself authorized the transaction,” and thus evade responsibility.

What to do in a panic? – Tips for Consumers

- If you ever find yourself in such a situation even a bank account suddenly emptied after a deposit, receiving suspicious calls/messages keep the following in mind:

- Do not call any links or numbers provided in text messages; call the number listed on the bank’s official website or statement.

- Monitor account activity immediately it’setter to catch small unauthorized transactions early.

- File a written complaint with the bank immediately, and keep copies of all correspondence.

- If the bank does not address your complaint,contact your state’s consumer protection department ordepartment or an organization like the Consumer Financial Protection Bureau (CFPB).

Why are such frauds increasing?

Nowadays, banking is not limited to branches; mobile apps, online check deposits, text alerts, andalerts, and phone banking all these have increased convenience butconvenience but also risks. Criminals confuse customers through fake texts and calls gaining trust by sending messages like, “Your account has been hacked.”

For example in this case, the message appeared to be from the bank, the caller sounded like a bank representative, and the customer acted accordingly. But in reality, it was a fraud.

Banking Institution’s Responsibility and Limitations

Banks implement several measures in the name of security alert systems, the option to freeze accounts, disabling debit cards, etc. but when the matter falls under the category of “customer consent,” the bank says, “We are not responsible.” The customer gets trapped in this situation In the U.S., this issue is further complicated because the regulations are outdated and the new types of digital transfers are challenging them.

Who receives the $1,000 stimulus payment on Thursday, October 23, 2025? Eligibility and requirements

Key Points of This Case

- The customer deposited a check at the bank branch this is a normal banking procedure.

- Nine hours after the deposit, a text message was received a message that appeared to be from the bank.

- A call was made to the number provided in the text message the call seemed legitimate.

- The next day, approximately $4,000 was missing from the account.

- The bank stated, “You authorized these transactions.” Therefore, we will not issue a refund.

- Later, after media reporting, the bank refunded some of the money (according to some sources).

Useful Information for Consumers

- Enable transaction notifications for your bank account right away, and check them consistently.

- Do not act immediately on text messages or phone calls that appear to be from the bank; check the bank’s website or app first to verify.

- Report suspicious messages or phone calls to the bank’s fraud department as soon as possible.

- If you see anything inappropriate right after a transaction, like a drop in funds, submit a written complaint to the bank immediately.

- Lastly, always keep a record of your communications with your bank; rename them if you must. This can pay dividends later.

Conclusion

This story isn’t just about one individual it’s about a system caught between customer protection and bank accountability. When customers place complete trust in their bank, incidents like this can be devastating to their financial security.

The case of Willie Delane provides a helpful reminder that while we should trust, we should also be cautious. Nowadays, banking is so much digital that everything can change with a click, a text message, or a phone call. Therefore, simply trusting a bank because of its name is not sufficient; we need to proactively take responsibility for our own safety.

If you’re interested to learn more about this I can share my interpretations of exactly what a bank is supposed to do, the perspective and response of industry regulators, and whether a standard of practice exists to address these issues in India. If you’d like, I’m also happy to draft an article on this topic.

FAQs

Q1. What happened to the Wells Fargo customer in this case?

A. A Wells Fargo customer reportedly lost over $4,000 just hours after depositing a check. When she filed a fraud claim, the bank denied responsibility, stating the transactions were authorized.

Q2. How did the fraud occur?

A. The customer received a fake text message and phone call that appeared to come from Wells Fargo. Believing it was legitimate, she followed instructions that allowed scammers to access her account.

Q3. Why did Wells Fargo deny the fraud claim?

A. Wells Fargo claimed that the disputed transactions appeared to be “customer-authorized.” This means the bank considered them valid, even though they were part of a scam.